63 / 84

63 / 84

0

100

200

300

400

500

600

700

800

61

Officelayout 169

aprile-giugno 2017

The office furniture sector in China

The Chinese firms increasing on the domestic market and slowing down on the international side.

The office sector to reorganize production activities to face high fragmentation

China office furniture business to face major

changes following increasing production

costs and competitive pressure from other

countries in the region like Indonesia and

Taiwan. According to the 2017 CSIL

analysis on a sample of over 100 Chinese

manufacturers the office furniture market is

trying to evolve to a more concentrated

business as outputs are still increasing

despite reduction is the number of

companies. The local Government support

the modernization through tax reductions

for companies that innovate production,

logistics and distribution systems.

The product evolution registered in China

over the last years is evident, however,

Nel corso del 2017 CSIL pubblicherà

le seguenti ricerche nel settore

del mobile per ufficio:

• “The European market for office furniture”

• “The office furniture market in China”

• “Office furniture: the world market outlook”

Maggiori informazioni sul sito

www.worldfurnitureonline.com2000

2000

2000

2000

200

455

755 700

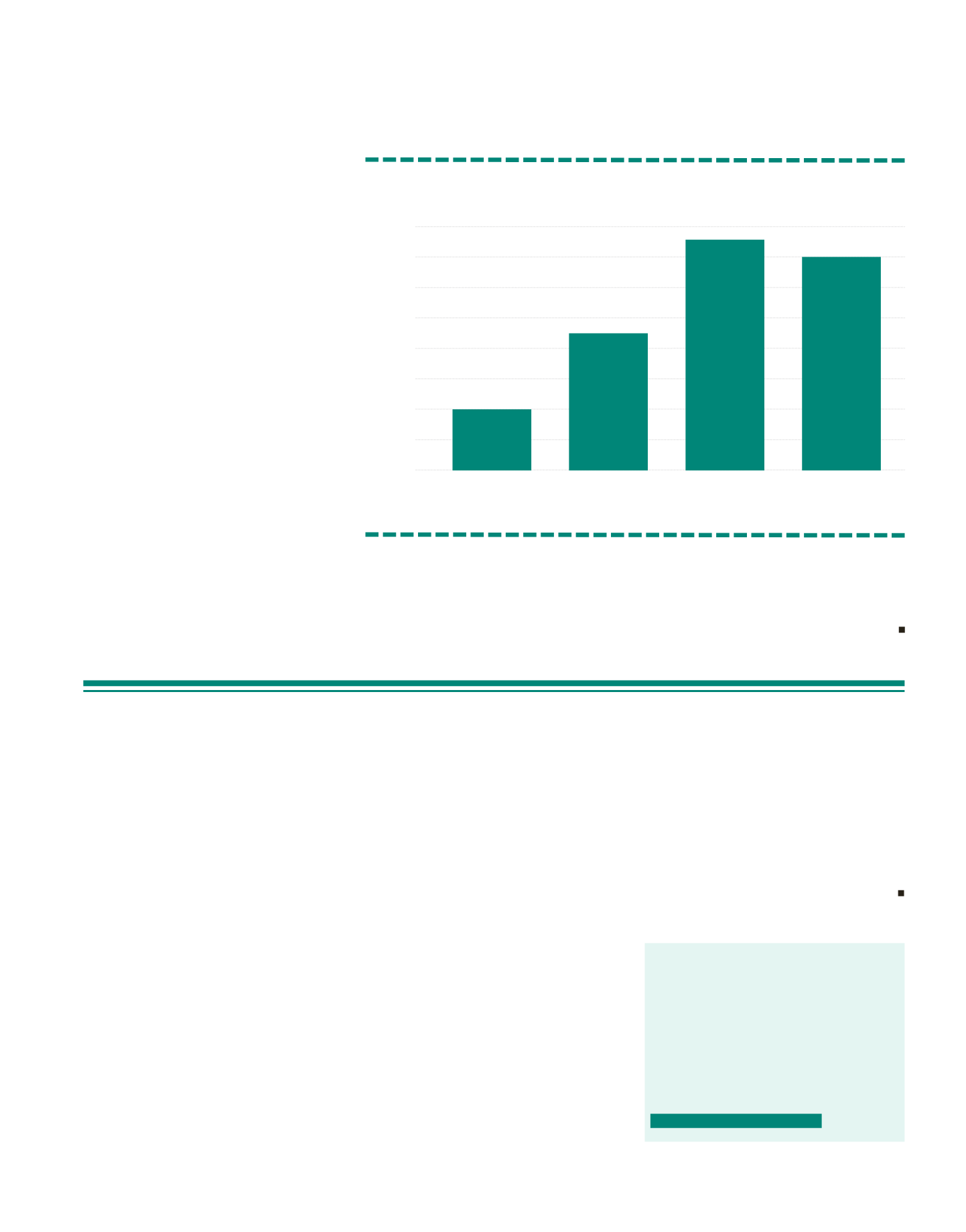

Cina. Distretto di Anji. Numero di imprese, 2005-2015

Fonte: CSIL su dati di fonte ufficiale

mercati internazionali visto che la quasi totalità

dei prodotti esportati sono realizzati in accordi

OEM (Original Equipment Manufacturing).

Nel 2016, per la prima volta dopo anni di cre-

scita ininterrotta le esportazioni di mobili per

ufficio cinesi hanno registrato un calo pari a cir-

ca il 6% (preliminare) sull’anno precedente. La

Cina resta comunque il principale esportatore

del settore, con un valore di circa 4 miliardi di

dollari essa rappresenta il 40% delle esporta-

zioni mondiali. Basti pensare che il valore delle

esportazioni cinesi è pari a 5 volte quello della

Germania. D’altra parte il ruolo predominante

della Cina come partner commerciale emerge

chiaramente anche osservando i dati dei prin-

cipali importatori mondiali per i quali essa è sta-

bilmente il primo fornitore.

Se le vendite sui mercati internazionali mo-

strano una riduzione, altrettanto non si può

dire per il mercato interno che continua a cre-

scere e a differenziarsi, seppur con una di-

namica meno accentuata rispetto al passato.

Secondo gli osservatori internazionali aumen-

ta sia la costruzione di nuovi spazi ufficio nelle

città emergenti sia i rinnovi e, quindi, la qua-

lità, delle superfici ufficio esistenti nelle “first

tier cities”. Alcune proiezioni (Fonte: JLL)

dicono che entro il 2020, Shanghai raggiungerà

oltre 11 milioni di metri quadrati di spazi ufficio

sorpassando Hong Kong. In crescita anche i

segmenti affini come quello degli ospedali e le

case di cura ai quali le aziende cinesi del settore

ufficio guardano con molto interesse.

local companies still lack of a “brand

identity” abroad as they supply

international customers mainly under OEM

agreements. Following years of

uninterrupted growth the exports of office

furniture reduced by around 6% in 2016

(preliminary).China remains the first

exporter of office furniture worldwide

posting a total value of USD 3.9 billion

(five times the export values of Germany),

equal to 40% of the world trade.

On the domestic front the market is still

healthy with increasing office surfaces

both in the first-tier metropolis and in the

second and third-tier ones. According to

JLL the total Grade A office space in

Shanghai will reach 11 million sqm by

2020, surpassing Hong Kong as the

largest office market in Greater China.